By Graeme Salt

This week’s budget made a number of key announcements, one of which was to remove negative gearing benefits for newly purchased properties except for brand new properties.

This difference between old and new will have a huge impact on your borrowing capacity due to the different way banks assess the impact of negative gearing on the household budget.

Some banks are very optimistic in their calculations of negative gearing benefits. And if these benefits will only apply to new properties, then the difference could be great.

I ran the numbers on a couple looking to buy an investment property which will rent out for $700 a week, let’s call them Sue and Steve. I assumed they:

- Both earn $100k

- Have no credit cards, nor HECS

- Pay $3,500 a month rent where they live

- Have modest living expenses

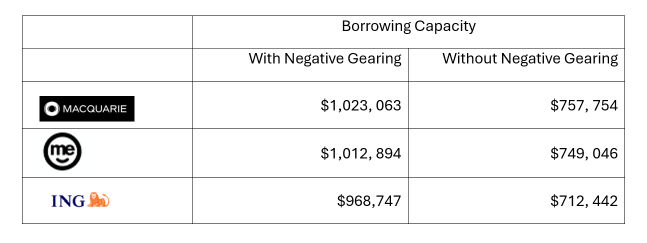

For some banks, the difference with and without negative gearing (and hence established versus new properties) is startling– see the table above.

These differences mean that many investors will probably focus on off-the-plan purchases – which is what the Treasurer wants.

But, how are the banks going to police this if negative gearing can only apply to new properties?

Normally, brokers arrange finance pre-approval before the borrower knows exactly which property they want to buy. Somehow, at some point, the banks will now have to do due diligence on the purchase to be sure it matches tax-wise.

Graeme Salt is an award-winning mortgage broker. For a no-obligations consultation on your home loan needs, please contact him on 02 9922 5055.