By Graeme Salt

This weekend auction clearance rate fell to 60.9 per cent, according to research house Cotality.

Such a low figure can imply there are more sellers on the market than buyers; often a pre-cursor to a price drop.

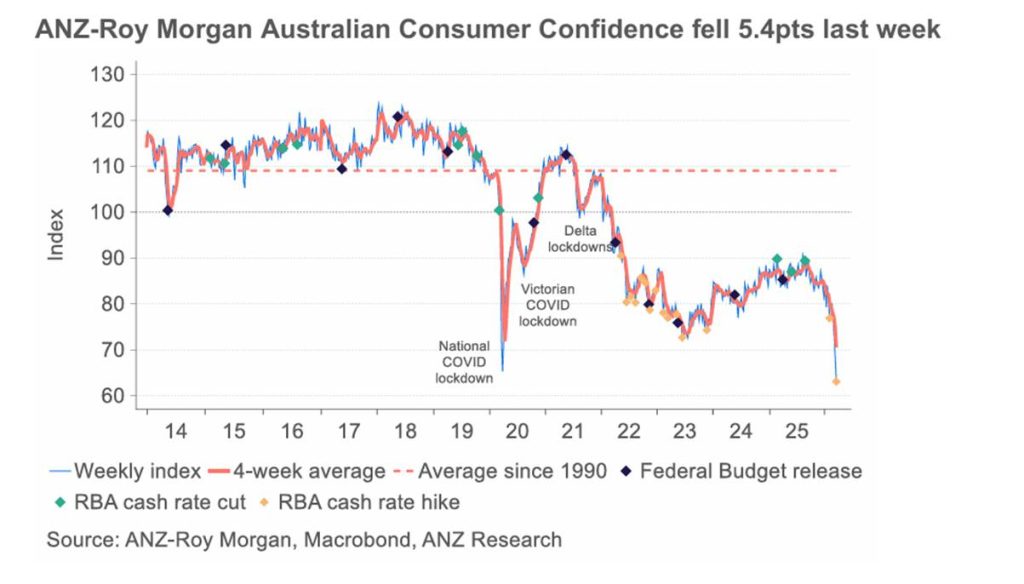

In the current climate (rate rises and Iran war) this is far from surprising. Such that the ANZ-Roy Morgan Consumer Confidence Index dropped 5.4 points to a record low – stretching back over 50 years since 1972 – below the previous COVID-19 pandemic low.

In this situation it’s hardly surprising that sellers are rushing their properties to market for fear of things falling further. At the same time, many buyers are moving to the sidelines, deferring any decisions until they see how the economic situation plays out.

And, with more rate rises forecast – uncertainty and a lack of confidence are the issues du jour.

But step back a bit and you will see, long-term, the Australian property market is likely to hold up.

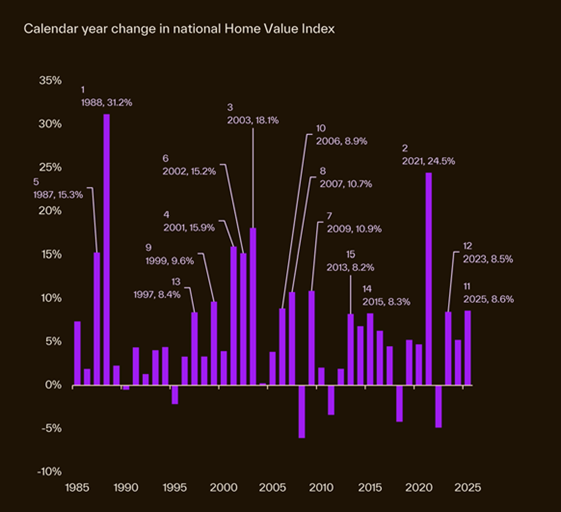

According to Cotality research, over the past four decades, there were only six years where home values fell. At most it was a 6.1 per cent drop in 2008 (GFC), the smallest was only 0.5 per cent in 1990.

And there are still economic drivers stimulating the property market and wider economy.

The First Home Guarantee Scheme is still making it feasible for first time buyers to get onto the property market – often in lower value properties.

And by the government’s own admission, we are still not building enough homes for our needs. According to Australian Bureau of Statistics (ABS) research, last year, the annual total of 179,040 commencements fell well short of the required 240,000 homes, resulting in a deficit of 60,960 new homes required.

For many property experts the next few months are just a (significant) blip in the property market.

Many savvy investors are keeping an eye out for bargains; knowing that inevitably prices will rise in the end.

Graeme Salt is an award-winning mortgage broker. For a no-obligations consultation on your home loan needs, please contact him on 02 9922 5055.