One big lever vs many smaller levers

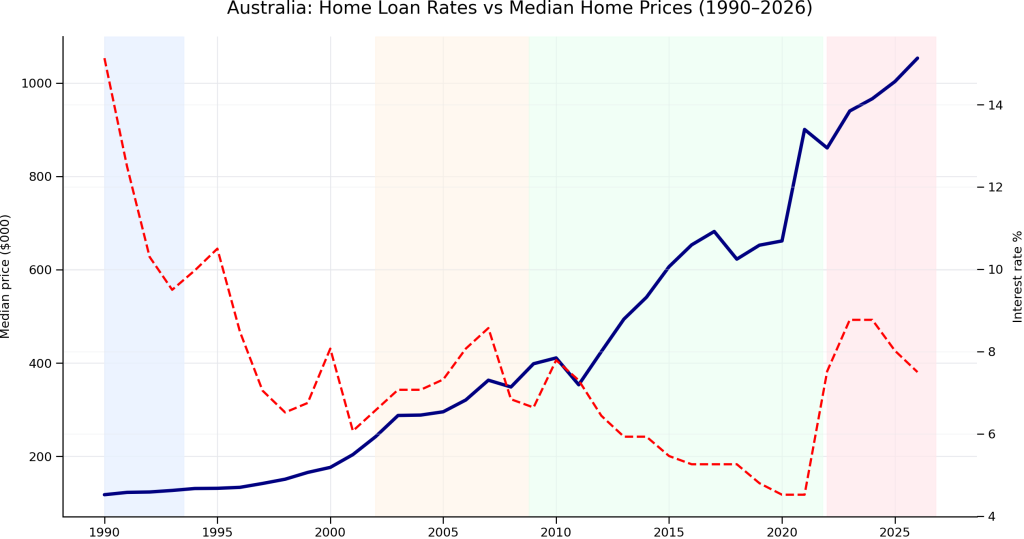

Today when people discuss property prices Australia, the debate often jumps straight to tax settings such as negative gearing or the CGT discount. Those settings likely contributed to investor demand, and they remain part of the picture. But if we are asking what best explains the broad, long-run rise in Australian property prices between 1990 and 2025, evidence suggests the bigger and more direct force was the long decline in interest rates and the resulting lift in borrowing power across the whole market.

That matters because lower rates do not just help investors. They affect owner-occupiers, first-home buyers, upgraders and refinancers as well. Tax settings are one influence, but rate settings change the maths for almost everyone who needs a loan. In a country where housing is heavily financed with debt, that makes rates the stronger economy-wide lever.

The long downtrend (1990–2025): Why the interest-rate backdrop matters

At a high level, the RBA cash rate is the interest rate on overnight funds between banks, and it acts as a benchmark for borrowing costs across the economy. Mortgage rates do not move one-for-one with the cash rate, but the cash rate strongly influences what lenders charge on home loans over time.

Australia’s rate backdrop changed dramatically over the period in question. In 1990, the cash rate was in the high teens; by November 2020 it had fallen to 0.10%, before rising sharply again from 2022 and sitting materially higher through 2025. That long downtrend from the early 1990s to 2020 lowered the cost of debt over decades, creating a powerful tailwind for housing values and other asset prices.

This does not mean property prices rose in a straight line. Australia experienced multiple property market cycles, with booms, pullbacks and long pauses. Different cities also behaved differently: Sydney and Melbourne often responded more sharply to credit conditions, while some regional markets were shaped more by local supply, lifestyle demand or employment trends. Even so, the national financing backdrop was set by the same broad interest-rate cycle. [rba.gov.au], [abs.gov.au]

Mechanism: Borrowing power is the bridge between rates and prices

The key link is borrowing power. When rates fall, mortgage repayments on a given loan size fall too. That means, for the same income and the same monthly budget, many borrowers can qualify for a larger loan and bid more for a home. If housing supply is tight, higher borrowing capacity often gets capitalised into higher prices.

Lenders do not assess loans only at the advertised rate. They test serviceability, meaning whether the borrower could still afford repayments if rates were higher. APRA currently requires regulated lenders to assess most borrowers using a buffer of 3 percentage points above the actual loan rate. This is meant to make the system more resilient to future rate rises.

In plain English, the mechanism looks like this:

- lower rates

- lower assessed and actual repayments

- higher borrowing capacity

- stronger bidding power

- higher prices, especially when housing supply is constrained.

A simple illustration helps. With a $4,000 monthly repayment budget, at 7% you might borrow around $600,000; at 4% you might borrow around $840,000. The exact numbers vary by loan term and lender policy, but the direction is the point: lower rates can materially increase what households can pay for the same property. That is why rates are such a powerful force in housing markets.

Where negative gearing and CGT fit (and where they don’t)

Negative gearing is when the costs of holding an investment exceed the income it produces, creating a loss that may be offset against other taxable income, such as salary and wages. In property, that often happens when rent does not fully cover interest and other deductible expenses.

The CGT discount is a concession that can reduce the taxable capital gain on eligible assets held long enough. For Australian resident individuals, the general rule has been that if the asset is held for at least 12 months, the capital gain can be reduced by 50% before tax is calculated. [ato.gov.au]

These settings likely contributed to investor appetite, especially for higher-income households expecting long-term capital growth. But they are not the only explanation, and they are not as broad in reach as interest rates. Tax settings mainly affect investors, and even then their impact depends on taxable income, expectations of future price growth, and whether lenders will actually extend the credit. Rates, by contrast, affect both investors and owner-occupiers through the price of debt and the size of loans they can service.

5. Why prices rose even outside investor-heavy periods

If tax settings were the main story, you would expect price growth to line up mainly with investor-heavy periods. But Australian housing values also rose during phases where owner-occupier demand was strong, because cheaper credit lifted borrowing capacity more broadly. ABS lending data continues to show large owner-occupier participation alongside investor activity, reinforcing that the housing market is not driven by one buyer type alone. [abs.gov.au]

Other forces also mattered and should not be ignored: income growth, population growth and migration, credit availability, sentiment, and persistent housing supply constraints. When demand rises faster than new homes can be delivered, prices can remain firm even if one demand source softens.

What changed in 2020–2025: Record lows, then rapid tightening

The 2020–2021 period gave Australians a real-time demonstration of the borrowing-power effect. The RBA cut the cash rate to 0.10% in November 2020, and mortgage rates fell to very low levels. That helped expand borrowing power and added fuel to housing demand.

Then the cycle turned. From May 2022, the RBA lifted the cash rate rapidly, taking it from 0.10% to 4.35% by late 2023, with 2025 still well above the pandemic lows. As rates rose, borrowing capacity fell and many borrowers faced sharply higher repayments. Yet prices did not collapse everywhere, which is a useful reminder that rates are powerful but not exclusive. Tight supply, solid population growth, wages, and expectations can keep prices resilient even in a higher-rate environment. Equally, prices can stall when rates fall if recession fears rise or lending standards tighten.

What this means for buyers, borrowers, and investors

For buyers and borrowers, the practical lesson is simple: focus not just on today’s rate, but on how rate changes affect your borrowing power, your mortgage repayments, and your cash-flow buffer. For aspiring brokers, this is also a core educational point: understanding serviceability, lender buffers and market cycles is central to explaining property finance credibly in Australia.

General information only: this article is educational and does not take your personal circumstances into account. Consider speaking with a licensed mortgage broker and a qualified tax adviser before making decisions involving borrowing or property tax outcomes.

What to do?

Over the long run, interest rates and property prices Australia have been closely linked because rates change the borrowing capacity of nearly every financed buyer. Negative gearing and the CGT discount likely contributed, but they are better understood as supporting influences rather than the main nationwide engine of price growth. The broader and more consistent explanation is the long decline in interest rates, transmitted through loan serviceability, repayment capacity and competition for limited housing stock.

If you are buying, refinancing or learning the broker profession, a sensible next step is to speak with an Origin Finance broker, review your borrowing power under different rate scenarios, compare variable versus fixed options, and build a buffer for future rate changes.

Call Origin Finance on 1300 30 6767 or

Contact | Origin Finance – Home Finance For Australians

✅ Frequently Asked Questions (FAQ)

What is the relationship between interest rates and property prices in Australia?

Interest rates and property prices in Australia are closely linked through borrowing power. Lower interest rates reduce mortgage repayments, allowing buyers to borrow more and bid higher for property. When this happens across many buyers, prices tend to rise—especially when housing supply is limited.

Why do lower interest rates increase property prices?

Lower rates reduce the cost of servicing a loan. This increases borrowing capacity, meaning more buyers can afford higher-priced homes. As competition increases, prices may rise. This borrowing-power effect is a key channel through which interest rates influence housing markets.

What is the RBA cash rate and why does it matter?

The RBA cash rate is the benchmark interest rate set by the Reserve Bank of Australia. It influences the interest rates that banks charge on home loans and other lending products. When the cash rate falls, mortgage rates typically fall over time, and vice versa.

How do lenders assess borrowing power?

Lenders assess borrowing power using serviceability, which looks at your income, expenses, and ability to repay a loan. They also apply a serviceability buffer, usually around 3 percentage points above the actual loan rate, to ensure you can afford repayments if interest rates rise in the future.

What is negative gearing in simple terms?

Negative gearing occurs when the costs of owning an investment property (such as loan interest and expenses) exceed the rental income it generates. The resulting loss can generally be used to reduce taxable income, depending on your circumstances.

What is the CGT discount?

The capital gains tax (CGT) discount allows eligible individuals to reduce the taxable portion of a capital gain—typically by 50%—if the asset has been held for at least 12 months. It is one of several tax settings that can influence investment decisions.

Are negative gearing and CGT discounts the main drivers of property prices?

Negative gearing and CGT discounts have likely contributed to investor demand, but they are not the only explanation for rising property prices. Interest rates tend to be a broader and more consistent driver because they affect borrowing power for both owner-occupiers and investors.

Do rising interest rates always cause property prices to fall?

Not always. While higher rates reduce borrowing power, property prices can still rise due to factors like limited housing supply, strong population growth, or wage increases. Property markets are influenced by multiple factors, not just interest rates.

Why did property prices rise between 1990 and 2025?

Several factors played a role, including income growth, population increases, housing supply constraints, and credit conditions. However, evidence suggests the long-term decline in interest rates helped increase borrowing power across the economy, supporting higher property prices over time.

What are housing supply constraints?

Housing supply constraints occur when new homes are not built quickly enough to meet demand. When more buyers compete for limited properties, prices can rise—even if other conditions, like interest rates, are changing.

What should buyers consider in a changing rate environment?

Buyers should consider:

- How interest rate changes affect their borrowing power

- Whether they can comfortably afford mortgage repayments

- The importance of maintaining a financial buffer

- Their loan structure (fixed vs variable)

Speaking with a mortgage broker can help clarify these factors.

Is now a good time to buy property in Australia?

This depends on individual circumstances, including income, deposit, borrowing capacity, and long-term goals. Market conditions vary across locations and property cycles. It’s important to assess your situation carefully and seek professional guidance.

Should I fix or stay variable on my home loan?

There is no one-size-fits-all answer. Fixed rates can provide certainty, while variable rates offer flexibility and may move with market cycles. Many borrowers use a combination of both. A broker can help compare options based on your goals.

Do interest rates affect refinancing decisions?

Yes. Changes in interest rates can affect the potential savings from refinancing, your borrowing power, and your loan structure. Reviewing your loan when rates change can help ensure it remains aligned with your needs.