In future, will people arrange their loans via AI – making brokers redundant?

The last few days, we have seen job losses in some of our major technology companies laying off:

- Block 4,000

- Atlassian 1,600

- Wistech 2,000

For Block, this represents 40 per cent of its workforce.

Most commentators argue that AI will impact white collar workers more than most – so I thought I would do some research to see if I will still have a business in a few years.

Here is what Copilot told me (I doubt ChatGPT or Claude would be that different).

In this case, Copilot did advocate for brokers. It did add:

So, to assess how far AI had developed with mortgages, I asked:

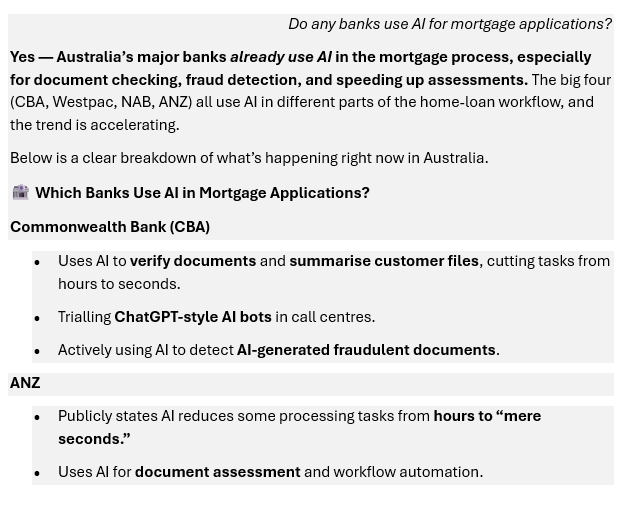

Copilot summarised that the banks are using AI for:

- Document verification

- Fraud detection

- Faster loan processing

Based on the above, it appears that AI assists brokers – rather than being a threat. But, if the technology allows individual brokers to put through more applications, maybe it will lead to consolidation within the industry and/or there will be less need for processing staff (both in Australia and overseas).

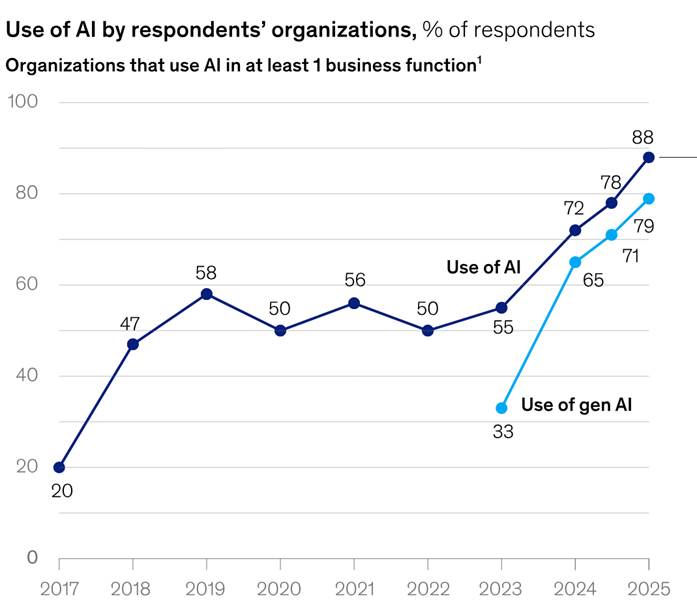

But AI is developing rapidly. According to McKinsey* 39 percent of organisations say they have begun experimenting with AI agents – capable of acting in the real world, planning and executing multiple steps in a workflow. This looks set to grow.

Currently, 76.8 per cent of mortgages are arranged through brokers. Right now, AI probably assists these figures.

But what happens when AI has the ability to ‘interview’ clients and give them feedback?

Comprehensive Credit Reporting means AI can analyse spending habits and (hopefully in a personable style) ask ‘do you really need to spend that much on UberEats 😉?

Let’s face it, if AI can develop applications like Rocky.ai that enable humas to focus on self-improvement and personal growth – surely it can do it itself?

Right now, brokers appear safe. Research by Colonial First State (CFSB) concluded that Australians still place a high value on professional advice and personal relationships when managing their finances; the more complex and important the task, the less comfortable they are relying on AI:

- 42 per for simple financial tasks such as budgeting, product comparisons or tracking spending

- 38 per cent AI for transactional banking activities such as managing everyday accounts or payments

- 29 per cent for investment management

The same probably also applies to credit – consumers are more likely to use AI to arrange less consequential loans such as car finance or personal loans – but will baulk at using the technology for buying a home.

In five years’ though, will it be the same? The CFSB research noted generational differences with younger Australians more comfortable with AI.

And 64 per cent of respondents said they believe AI will become a common feature of financial services within the next five years

But might Australians adapt such that, in the future, even buying a home (one of our most important investments) is something we feel comfortable arranging via some form of agent?

*McKinsey: The state of AI in 2025: Agents, innovation, and transformation