‘Life will never be the same again.’ Its been said non-stop since Coronavirus, but there is no doubt it has accelerated long overdue changes in the property market.

Across the board, property-related professions are adapting and thriving despite the virus.

Over the weekend, 73 per cent of Australia’s capital city auctions were successful, according to CoreLogic.

Of these, Melbourne achieved a 60 per cent clearance rate – despite the Covid-19 lockdown. Given that auctions must now be held at an auctioneer’s home, rather than at agency offices this is an impressive performance.

Buyers are learning the art of bidding for a property online.

But online activities don’t just stop there. Necessity is the mother of innovation and the banks have been forced to adapt; NAB recently announced cuts at 115 branches across regional Australia as it increasingly replaces face-to-face interactions with phone and online services.

Other banks too are adapting to online mortgages; where once borrowers and brokers were forced to have face-to-face meetings, banks are increasingly accepting brokers having identified borrowers via Zoom or Skype for example.

Covid-19 is having a huge impact on Australia’s geography with many professionals (and their bosses) realising that they don’t have to be in the CBD office every day; instead they can choose to live in lifestyle locations such as NSW’s Central Coast or the Sunshine Coast – locations that increasingly lack bank branches, making the role of the mortgage broker all-the-more important in a post Covid world.

https://originfinance.com.au/origin/wp-content/uploads/2020/03/Coronavirus-financial-markets.jpg9001200Graeme Salthttps://originfinance.com.au/origin/wp-content/uploads/2014/12/origin-finance-logo.jpgGraeme Salt2020-08-18 12:09:372023-05-22 15:19:35How Covid-19 Transformed the Property Market

Covid-19 has turned property demand such that new research maps ‘Danger Zones’ in the propertly market.

COVID-19 has led to an immediate (if perhaps temporary) shift outwards in the demand for housing, such that experts have identified two risks property owners face.

In some location there is now the risk of negative equity (where a house is worth less than the mortgage).

And COVID-19 has increased properties’ cash-flow risk, with vacancy rates at an all-time high in May at 16.2 per cent.

Riskwise Property Research has produced research showing Australia’s Top 10 Danger Zones

The table below lists the riskiest areas in the country in terms of oversupply, based not only on the supply itself but also on low demand for rental apartments.

State

Post code

Suburb

New units next 24 months

New units next 24 months as % of units

VIC

3000

Melbourne

4,744

13.6%

VIC

3008

Docklands

1,307

12.0%

NSW

2020

Mascot

804

13.3%

NSW

2155

Rouse Hill

1,661

200.4%

NSW

2150

Parramatta

1,553

13.2%

NSW

2250

Gosford

1,859

72.9%

NT

800

Darwin

1,204

32.0%

QLD

4101

West End

1,211

26.0%

QLD

4217

Surfers Paradise

2,779

14.0%

SA

5000

Adelaide

1,266

12.9%

Many of these risky locations are at the confluence of inner-city locations and off-the-plan purchases

According to CoreLogic, the portion of stock advertised across Melbourne saw a large jump from 3.2 per cent of listings advertised in April, to 3.6 per cent over May, representing a total rent listing uplift of more than 3,000 across Melbourne, up to about 27,000 properties for rent over the month, corresponding to a rise in vacancies and falling rental prices.

In Sydney, Mascot is still reeling from the effects of oversupply alongside construction defects where during the December 2019 quarter prices fell 4.6 per cent to $880,000.

Surprisingly, Gosford entered RiskWise’s 2020 list of Top 10 Danger Zones largely due to oversupply of units (at more than 72 per cent of existing stock) plus the fact that many of these units are unsuitable for families.

In Queensland’s Surfers Paradise, where houses with pools are the preferred option for residents, the unit market has taken a hit as COVID-19 materially impacts the tourism industry.

Rental values have also slumped across the country, according to CoreLogic falling 0.5 per cent in the June quarter – the sharpest decline in two years. In addition, unit rents have been hit the hardest with falls in both Sydney and Melbourne of 2 per cent over the past three months.

https://originfinance.com.au/origin/wp-content/uploads/2019/12/bruce-mars-AFaMbjb9sDM-unsplashres.jpg16892368Graeme Salthttps://originfinance.com.au/origin/wp-content/uploads/2014/12/origin-finance-logo.jpgGraeme Salt2020-08-18 12:06:492023-05-22 15:19:36Australia’s Top 10 Oversupply Areas

Property prices are expected to rise 10 per cent over 2020

as low interest rates entice buyers back into the market.

The pace of growth will ease in the second half of the year

as more and more housing becomes unaffordable for increasing numbers of people.

Faced with weak wages growth and a rising unemployment rate, heavily indebted Australians will struggle to afford homes when prices reach a certain point.

But that’s not to say the boom is ending any time soon.

AMP Capital senior economist Diana Mousina said there is

still enough demand to drive prices in Sydney and Melbourne to new record highs

within months.

Ms Mousina said in a note to clients that AMP expected “national

home prices to increase by around 10 per cent in 2020”.

SQM Research has similar forecasts.

“After 2020, we expect price growth to be more moderate,

around 5 per cent per annum,” Ms Mousina wrote, adding that the recent run up

in debt didn’t yet pose a risk to financial stability.

The current upswing started in Sydney and Melbourne when the

Reserve Bank cut rates in June.

Price increases were modest at first.

But another two rate cuts and an easing of serviceability standards kicked things up a gear, with the lift in values eventually spreading to all other capital cities.

As of January 31, property analytics firm CoreLogic said national prices had lifted 6.7 per cent since finding their trough, with the median in Sydney and Melbourne coming in at $862,814 and $681,925 respectively.

Ms Mousina said record-high debt levels and tighter lending

standards would conspire with tough economic conditions and an increased supply

of units to take some heat out of the market.

But low interest rates and the prospect of further cuts will

outweigh these factors.

And sluggish building approvals point to supply shortages in

the near future, meaning prices could get another boost down the track.

“Building approvals need to be running around 18,000 per month to keep up with demand, which remains high because of migration. However, approvals are only tracking at around 15,000 per month,” Ms Mousina wrote.

“The risk is that housing demand will start to track above new supply again which will push vacancy rates down and put upward pressure on home prices and rents again.”

Ms Mousina said governments had a role to play in ensuring

the supply of housing met demand, “especially through land release”.

Germany could provide some pointers, she said.

The European nation tends to build more homes than Australia

as their governments set targets for the supply of new housing, whereas

Australia’s “discretion-based system” gives local residents the power to stop

new projects from getting off the ground.

The use of this veto power is often referred to as NIMBYism,

or not-in-my-backyard-sentiment.

AMP’s revised housing forecasts come as the Australian Bureau of Statistics announced on Wednesday that the value of total construction work done fell 3 per cent over the last quarter of 2019.

The value of completed work was 6.6 per cent lower than the

year before.

Ms Mousina said the construction downturn alone would

detract one percentage point from this year’s GDP.

Westpac senior economist Andrew Hanlan described the figures

as “a weak end to what was a weak year for the sector”.

“Disruptions from the bushfires may have added to the

weakness in the quarter – although it is notable that sizeable falls were

evident in all states,” Mr Hanlan wrote.

“As to implications for broader economic growth, with the

construction sector representing around 13 per cent of the economy, the 3 per

cent drop in work in the December quarter will have a material direct impact.”

And that was before the coronavirus.

Search real estate for sale or rent anywhere in Australia

from licensed estate agents on simply type in any suburb in the search bar

below

https://originfinance.com.au/origin/wp-content/uploads/2020/03/white-android-tablet-turned-on-displaying-a-graph-186464-1.jpg12801920Graeme Salthttps://originfinance.com.au/origin/wp-content/uploads/2014/12/origin-finance-logo.jpgGraeme Salt2020-03-01 10:15:042020-07-15 21:02:14House prices set for double-digit growth: AMP

Interest rates are on hold for now, but another cut is likely coming.

The Reserve Bank of Australia (RBA) announced on Tuesday that it had kept the official interest rates at 0.75% at its February meeting.

“With interest rates having already been reduced to a very low level and recognising the long and variable lags in the transmission of monetary policy, the Board decided to hold the cash rate steady at this meeting,” RBA Governor Phillip Lowe said in a statement.

Lowe and the rest of the RBA board seem satisfied for now that record low-interest rates are doing enough to stimulate Australia’s economy.

“The easing of monetary policy last year is supporting employment and income growth in Australia and a return of inflation to the medium-term target range. The lower cash rate has put downward pressure on the exchange rate, which is supporting activity across a range of industries,” Lowe said.

“Lower interest rates have assisted with the process of household balance sheet adjustment. They have also boosted asset prices, which in time should lead to increased spending, including on residential construction. Progress is expected towards the inflation target and towards full employment, but that progress is expected to remain gradual.”

While largely in line with expectation, a small number of economists have begun to suspect the RBA might not be as predictable as assumed.

Around one in ten economists had thought the official cash rate would be cut on Tuesday, according to a Bloomberg survey. But despite the broad consensus, there are a growing number of contrarians who doubt the decision remains quite so black and white.

Economists from banks ING, Deutsche and Morgans were all betting on a cut to 0.5%, which would constitute another record low. Given the ongoing, and as yet unquantified, economic damage the bushfires and now the coronavirus will wreak, the RBA could have been inclined to move preemptively.

“[It’s] splitting the difference between what the market thinks and what the RBA thinks,” Morgans analysts wrote in a note issued to Business Insider Australia before the decision. “The RBA thinks the economy is in pretty good shape, the market thinks it’s in need for help, so we forecast one further rate cut but it’ll stabilise there.”

On the other, more popular, side of the debate were all big four Australian banks, flanked by AMP Capital, HSBC, JP Morgan, Morgan Stanley, and UBS. Of those, only UBS and and AMP are pricing in a March cut. The big four are instead anticipating, with the current data, the RBA will wait until April to make an orderly move lower.

“It would be a genuine surprise [if the RBA cut in February]” IFM Investors economist Alex Joiner tweeted. “Data [hasn’t] thrown up any red flags and I personally wouldn’t think near term weakness from exogenous factors will be enough for the RBA to spend the limited policy space it has left.”

Better looking economic indicators heading into the end of 2019 have helped steady market jitters. A fall in the unemployment rate — a key RBA objective — in December helped alleviate some of the pressure for rates to be slashed once again.

“A further gradual lift in wages growth would be a welcome development and is needed for inflation to be sustainably within the 2–3% target range,” Lowe said. “Taken together, recent outcomes suggest that the Australian economy can sustain lower rates of unemployment and underemployment.”

However, even while analysts thought there wasn’t a pressing enough case for an immediate cut, they wouldn’t rule it out amid threats to Australian economic growth.

“While we are not calling for an RBA rate cut until April, there is a risk of a rate cut at today’s meeting,” Commonwealth Bank chief currency strategist Richard Grace said in a note. “The RBA is likely to refer to the coronavirus in their accompanying monetary policy statement.”

While the RBA board did, in fact, refer to the coronavirus, it’s keeping its cards close to its chest, acknowledging the outbreak will only “temporarily weigh on domestic growth.”

With the February decision out of the way, analysts will now cast their eyes forward. The market had been pricing in a 50% probability of an April cut and 65% of one in May instead. While consensus may have doubted a February cut, the majority of economists expect the RBA will be forced to cut to 0.5% soon.

Exactly when however is anyone’s guess.

https://originfinance.com.au/origin/wp-content/uploads/2014/12/origin-finance-logo.jpg00Graeme Salthttps://originfinance.com.au/origin/wp-content/uploads/2014/12/origin-finance-logo.jpgGraeme Salt2020-02-04 15:13:312020-07-15 21:02:15The RBA has kept the official interest rate on hold at its February meeting, but speculation is rife when the next cut is coming

Australian house prices continued to rise in January, with increases spreading beyond the booming Sydney and Melbourne markets.

The big south-eastern cities continued to lead price rises, but all other capitals posted gains, including modest 0.1 per cent increases for the struggling Perth and Darwin markets.

However, the top 10 capital-city price increases were in areas of Sydney and Melbourne, while six of the 10 biggest falls were in Perth and its surrounds.

Regional Tasmania had the three strongest areas for price growth outside the capitals, while outback Queensland and WA led regional declines.

Overall, CoreLogic’s figures show the pace of growth has slowed from peaks during the spring selling season, with capital city prices rising 0.9 per cent on average, while regional markets typically posted a 0.7 per cent increase.

“Factoring in the seasonal effect, the latest results indicate a reduction in the speed of growth across most markets, especially for Sydney and Melbourne where affordability constraints are once again becoming more pressing,” CoreLogic’s head of research Tim Lawless said.

“We were seeing values rising by nearly 3 per cent back in November month-on-month in Sydney.

“That growth rate is now reduced down to 1.1 per cent, and Melbourne’s reduced from a peak monthly rate of 2.3 per cent in October down to 1.2 per cent in January.

“So I think we are seeing the effects of worsening housing affordability and maybe some early signs that higher stock levels on the market are starting to dampen this very high rate of capital gain.”

Mr Lawless expects that weaker trend in price growth to continue as an increasing number of property owners take advantage of a rising market to sell.

“Our expectation is that through the March quarter we probably will see listing numbers rising much more substantially as we see home owners taking advantage of what have been quite strong selling conditions,” he told ABC News.

Nationally, housing values have rebounded 6.7 per cent since reaching a low point in June last year, but they are still 2.2 per cent below the most recent peak in October 2017.

Despite this, falling rents mean the return for property investors in Sydney is at a record low of 3 per cent, while the yield in Melbourne is also very low at 3.2 per cent.

Nationally, rents increased by just 1.3 per cent over the past year — below inflation and wage growth, with Hobart (+5.8 per cent) the only capital where rents were increasing substantially faster than incomes.

However, CoreLogic also noted the average three-year fixed mortgage rate for investors was 3.48 per cent, meaning landlords in many Australian capitals could be making positive returns, while it may be cheaper for people in some capital cities to meet mortgage repayments than pay rent.

https://originfinance.com.au/origin/wp-content/uploads/2014/12/origin-finance-logo.jpg00Graeme Salthttps://originfinance.com.au/origin/wp-content/uploads/2014/12/origin-finance-logo.jpgGraeme Salt2020-02-04 14:56:092020-07-15 21:02:15House price rises spread beyond Sydney and Melbourne, but pace of growth slows

Soaring property prices “are yet to crush the home ownership dreams of first-home buyers,” says ME Bank.

But they aren’t doing much for the broader economy.

Interest rate cuts and looser bank lending have seen national housing prices rise more than 5 per cent since finding their trough in July.

The strength of the rebound has surprised many analysts and prompted economists to sound the alarm over rising household debt.

But ME’s latest Quarterly Property Sentiment Report found the return of the property boom hasn’t dulled the ambitions of aspiring home owners – even though ABS figures show they are gradually being priced out of the market.

More than half of would-be home owners (51 per cent) plan to buy property over the next 12 months, according to ME Bank’s survey, which canvassed 1000 Australians at the start of January.

Source: ME Bank Quarterly Property Sentiment Report

ME Home Loans general manager Andrew Bartolo said this showed rapidly climbing prices were instilling a sense of urgency among first-home buyers and had yet to crush their dreams of home ownership.

“In the case of first-home buyers, the recent property price recovery has likely nudged them to get in while they can – as though it’s now or never,” Mr Bartolo said.

“Low interest rates and commentary in the market for the support of first-home buyers may have also contributed to an increase in home-buying intentions,” he added, referring to the Coalition’s first-home buyer scheme.

The report shows attitudes towards the property market have improved for the third consecutive quarter, increasing three percentage points since the last survey to a net positive (i.e. positive sentiment minus negative sentiment) of 21 percentage points.

Home owners are less concerned about negative equity, too, and reported improved confidence in their general finances.

But more than nine in 10 Australians (92 per cent) believe that housing affordability is still “a big issue in Australia”.

And rising property prices are discouraging spending more than encouraging it.

Source: ME Bank Quarterly Property Sentiment Report

ME’s findings mirror those of other recent reports.

While devastating bushfires pushed consumer confidence to one of its lowest levels since the GFC, expectations of rising house prices increased 8.1 per cent in the monthly Westpac-Melbourne Institute consumer confidence index.

The sharp jump in house price expectations came after Commonwealth Bank reported that home-buying intentions hit record levels in December, while retail spending intentions flatlined.

“Households remain very happy to spend on housing. But they remain very cautious about spending at the retail level,” CBA chief economist Michael Blythe said at the time.

“And within the overall consumer mix, the preference is to spend on experiences over goods.”

ME’s report found something similar.

Although attitudes towards the property market are continuing to improve, Australians’ “willingness to spend on discretionary items” dropped five percentage points over the quarter to a net negative of eight percentage points.

Mr Bartolo said this showed rising property prices had yet to deliver a positive “wealth effect” to consumers.

Source: ME Bank Quarterly Property Sentiment Report

Meanwhile, EY chief economist Jo Masters told The New Daily the ongoing house price rebound delivers a weaker wealth effect than past house price recoveries for two reasons.

Firstly, Australians are heavily indebted and have shown a preference for paying off debt rather than spending.

And, secondly, the memory of the recent downturn is still fresh in people’s minds, meaning home owners might place less faith in the sustainability of the recent price surge.

Ms Masters said prices are likely to rise at a slower pace this year, too.

More vendors will want to sell their homes after months of price increases, meaning supply will rise to meet demand, and fewer people will be able to afford a home the longer the rebound goes on for.

“And then for first-home buyers, it’s still an incredibly challenging environment,” Ms Masters added.

“In the last housing finance numbers, it looked as if the pace of first-home buyer approvals was coming off, but the average size of the mortgages being given to first-home buyers was rising, which is consistent with prices going up.

“So it does look like prices have risen to a point where … first-home buyers are a little bit more overstretched and taking longer to get their financing in place.”

Economic growth will take a 0.3 percentage point hit over the December and January quarters due to Australia’s bushfire crisis, according to the latest analysis from Goldman Sachs.

But could it be the bushfires actually have an economic stimulus?

Devastation is rightly used to describe the impact on those individuals and communities affected by the fires. But could they have a positive impact on the economy?

Both the public and private sectors are likely to be pumping a significant amount of dollars into locations affected by the economy, for example:

The Federal Government has announced a $2bn National Bushfire Recovery Fund

The NSW government has announced $1bn infrastructure package fire-affected communities

Suncorp and IAG have received $345m and $160m of bushfire-related insurance claims

Once these funds start to flow into these communities, they will have a significant impact on the local economies. In six-months’ time, it may be hard to get hold of a tradie because they will be working on some of the reconstruction projects.

And while no-one would ever wish these events on anyone, Doctors and pharmacists are likely to be very busy over the next few months, assisting the recovery.

Here in, lies the rub – we see lots of negative headlines about the economy. But the picture is probably stronger (but by no means sublime) than the media lets on.

This week retail sales figures came out that were better than expected. Seasonally adjusted retail sales surged 0.9 per cent in November, surprising economists who had expected just 0.4 per cent growth.

And Australia recorded its 23rd consecutive monthly trade surplus after stronger coal, iron ore and gas exports saw a $1.7 billion jump to a better than expected $5.8 billion in November, but imports have slowed – sparking concerns about consumption.

The importation of goods and services fell 3 per cent or $1 billion in November. Consumption goods fell 7 per cent or $610 million.

To cap off the bad news, ANZ’s monthly Australian job ads survey, fell 6.7 per cent in December in seasonally adjusted terms – partly due to the bush fires.

But with the Reserve Bank likely to drop interest rates further and cash to be splashed across much of NSW, VIC and SA, local economies are likely to be boosted.

None of us ever want to see these bushfires again. But we may come back from them stronger than before.

https://originfinance.com.au/origin/wp-content/uploads/2020/01/graeme-salt-bushfire-2.jpg673886Graeme Salthttps://originfinance.com.au/origin/wp-content/uploads/2014/12/origin-finance-logo.jpgGraeme Salt2020-01-10 15:11:502023-05-05 13:25:43Bushfires to have a positive economic impact

As home values sharply recover in Sydney and Melbourne, there has been a particular spike in the recovery of the premium housing, according to new research.

According to the November Home Value Index, released by property analytics company CoreLogic, the value of properties sold across Australia in the month ending 30 November 2019, grew by 1.7 per cent – the largest national monthly gain since 2003.

While the report shows this uptick has been particularly driven by the Sydney and Melbourne markets, the report also reveals that the recovery has been particularly noticeable in the upper quartile of the market.

Building on a trend highlighted in October, it is the more expensive properties that are driving the value rebound.

Looking at the figures over the past three months, values across Sydney’s top quartile were up 7.4 per cent over the three months ending November, compared with a 3.8 per cent rise across the lower quartile.

Meanwhile, in Melbourne, top quartile values were up 8.1 per cent over the same three-month period compared with a 4.2 per cent rise across the lower quartile.

Brisbane, Perth and Darwin were also recording a similar trend where premium value properties were outperforming lower value properties in the three-month period.

While housing values are rising across each of the valuation cohorts, the recovery trend is most concentrated within the premium sector of the market, CoreLogic’s head of research, Tim Lawless, said.

“This trend is most evident in Sydney and Melbourne where the top quartile of the market is outperforming the broad ‘middle’ of the market and lower quartile,” he said.

“The stronger performance across the higher value end of the market can likely be attributed to a combination of values falling more in this sector during the downturn, as well as recent adjustments to serviceability rules which has boosted borrowing capacity.

“Additionally, the scarcity value of detached homes in many of the blue-chip property markets is another factor supporting strong capital gains.”

Mr Lawless concluded: “As housing values become less affordable in these high-end markets, demand is likely to ripple outwards to the more affordable areas.”

As previously reported, CoreLogic’s Home Value Index for the month ending 30 November showed a steep recovery in home values over the month.

Sydney dwellings saw monthly growth of 2.7 per cent – the largest month-on-month gain it has seen since 1988, while Melbourne properties saw their strongest growth since 2009 (2.2 per cent), taking it back to similar growth levels as the peak in 2012-17.

Mr Lawless told Mortgage Business: “This really highlights how fast this rebound has been in those two markets, and I think we will probably see growth continuing into early 2020 while supply levels remain very low, which is creating quite a bit of urgency in the market.”

https://originfinance.com.au/origin/wp-content/uploads/2014/12/origin-finance-logo.jpg00Graeme Salthttps://originfinance.com.au/origin/wp-content/uploads/2014/12/origin-finance-logo.jpgGraeme Salt2019-12-14 15:35:022019-12-14 15:42:58Value recovery driven by expensive houses

People selling a house in a uniquely-named street name could add thousands of dollars to the sale price, new research shows.

Academics from Deakin University, National University Singapore and the Chinese University of Hong Kong found that Sydneysiders had a preference for longer, one-word street names in their recent study, Street Name Fluency and Housing Prices.

House buyers wanted unique street names, the research found, with houses in those streets reporting statistically higher sales prices – by 1.4 per cent or $9481.

Deakin University Associate Professor of property and real estate Adrian Lee said uniquely named streets were highly prized by property buyers.

“People want something different – names that are not commonly used in Australia,” Associate Professor Lee said.

“Royal names are sought after, so King George Street, not just regular George Street, or Prince William, not just regular William,” he said.

The study showed that besides royal names, words related to popular celebrities or trendy terms may be preferred in street names, with buyers attaching a premium for houses on those streets.

That included Brock Street, which was particularly of interest after the death of famous Australian race car driver Peter Brock.

While unique street names were attractive throughout the year, festively-named streets could appeal to people, particularly at Christmas time.

Across Victoria, land, houses and apartments were currently for sale in streets, including Noel Street, Wreath Drive and Angel Street.

Selling a property on a festively-named street could also work for people selling at Christmas time, Associate Professor Lee said.

US studies had shown that some people “projection buy” that is, they buy according to the season, which means the time of year can influence their buying habits.

“It may happen with Christmas. It’s possible they could buy a house in a street like that because it’s Christmas and then perhaps have buyer’s remorse afterwards,” he said with a laugh.

With only two major auction weekends left before Christmas, agents and vendors are hopeful for more sales.

Kay & Burton Armadale partner Michael Armstrong said while properties in the middle and lower price brackets had sold well throughout the second half of the year, more expensive properties had been quieter with fewer being put up for sale.

He expected that sales at all price brackets would be solid until the end of the year.

“I think there will still be a lot of people wanting to get in and buy a house,” Mr Armstrong said. “It seems like there’ll be successful sales right up until Christmas.”

https://originfinance.com.au/origin/wp-content/uploads/2014/12/origin-finance-logo.jpg00Graeme Salthttps://originfinance.com.au/origin/wp-content/uploads/2014/12/origin-finance-logo.jpgGraeme Salt2019-12-14 15:30:462019-12-14 15:44:23Why you should try selling a home in a festively-named street at Christmas

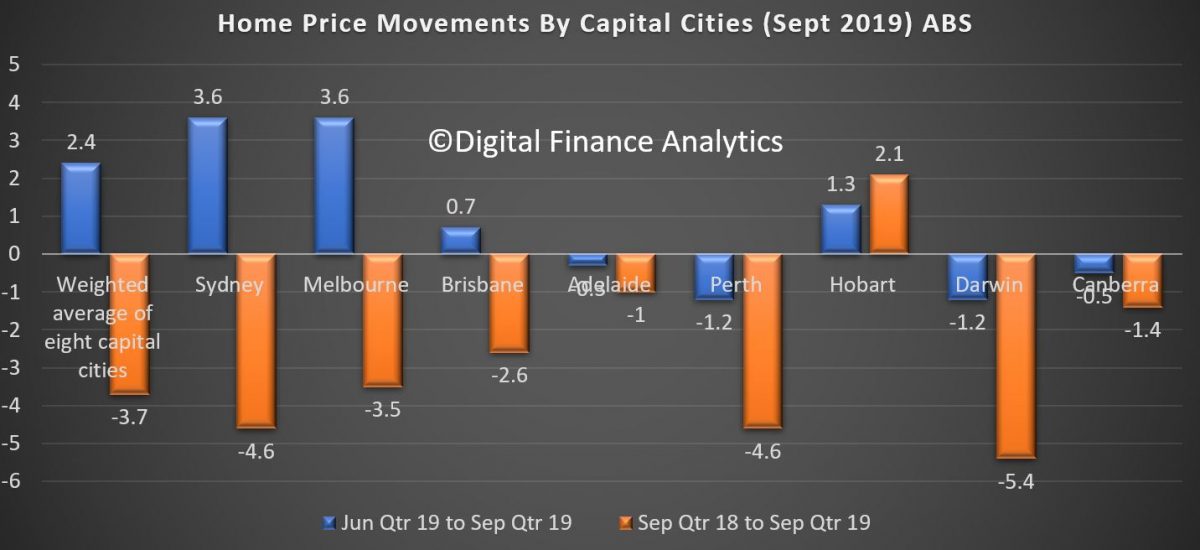

Martin North| Digital Finance Analytics|10 December 2019

Residential property prices rose 2.4 per cent in the September quarter 2019, the strongest quarterly growth since the December quarter 2016, according to figures released today by the Australian Bureau of Statistics (ABS).

Sydney and Melbourne residential property prices recorded strong growth in the September quarter 2019. Property prices rose in Sydney (+3.6 per cent), Melbourne (+3.6 per cent), Brisbane (+0.7 per cent) and Hobart (+1.3 per cent).

House prices rose 4.0 per cent in Sydney and 3.7 per cent in Melbourne while attached dwelling prices rose 2.8 per cent in Sydney and 3.6 per cent in Melbourne.

ABS Chief Economist Bruce Hockman said, “The increase in property prices is in line with housing market indicators, particularly in Sydney and Melbourne. New lending commitments to households, auction clearance rates and sales transactions all improved during the September quarter.”

Residential property prices fell 3.7 per cent in the year to the September quarter 2019, with all capital cities except Hobart recording falls. This is a noticeable improvement on the 7.4 per cent annual fall in the June quarter 2019.

The total value of Australia’s 10.4 million residential dwellings rose by $189.9 billion to $6,869.4 billion in the September quarter 2019. The mean price of residential dwellings in Australia is now $660,800.

https://originfinance.com.au/origin/wp-content/uploads/2014/12/origin-finance-logo.jpg00Graeme Salthttps://originfinance.com.au/origin/wp-content/uploads/2014/12/origin-finance-logo.jpgGraeme Salt2019-12-14 15:28:062019-12-14 15:45:23Sydney and Melbourne Drive Property Price Rise of 2.4% In September Quarter – ABS

Origin Finance is a

Origin Finance is a